Here’s a fun fact: At PayPal’s peak valuation of USD 340 billion, it would have been worth more than Bank of America (USD 248 billion) and Citigroup (USD 88 billion) COMBINED. So why is PayPal down by so much now?

Early PayPal investors received a rude shock when the stock experienced a near 80% decline — from a high of over $300 per share in 2021, it has crashed down to near $60 per share in 2023.

Investors are wondering if it’s a good time to bargain hunt, or whether this might turn out to be a classic value trap.

Sit tight and strap in. We’ve got many insightful deliberations to share from our deep-dive research.

Table of Contents:

Why is PayPal Stock Down by 80%?

PayPal Stock Analysis: Business Fundamentals

Will PayPal Stock Go Up? My Problems with PYPL Today

Why Is PayPal Stock Down by 80%?

First things first, I think it would be helpful to understand the background of PayPal’s price action. Why did PayPal stock drop by 80%?

PayPal’s Growth Disappoints

The PayPal of 2021 is vastly different from the PayPal of 2023. In recent times, we can observe clear signs of weakness in PayPal’s fundamental business dealings.

First, on revenue and earnings growth.

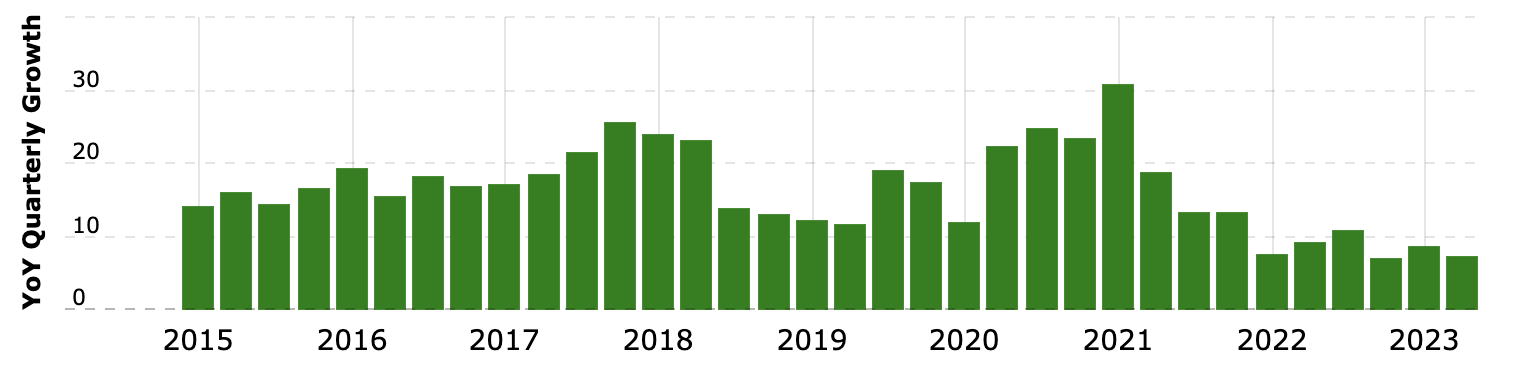

Source: Macrotrends, PayPal’s Revenue Growth

Pre-2022, PayPal was able to easily sustain their top-line revenue growth rate by double digits, sometimes even pushing over 20% YoY growth. However, post-2022, we can see clear signs of slowdown and they have managed to deliver only high single-digit growth.

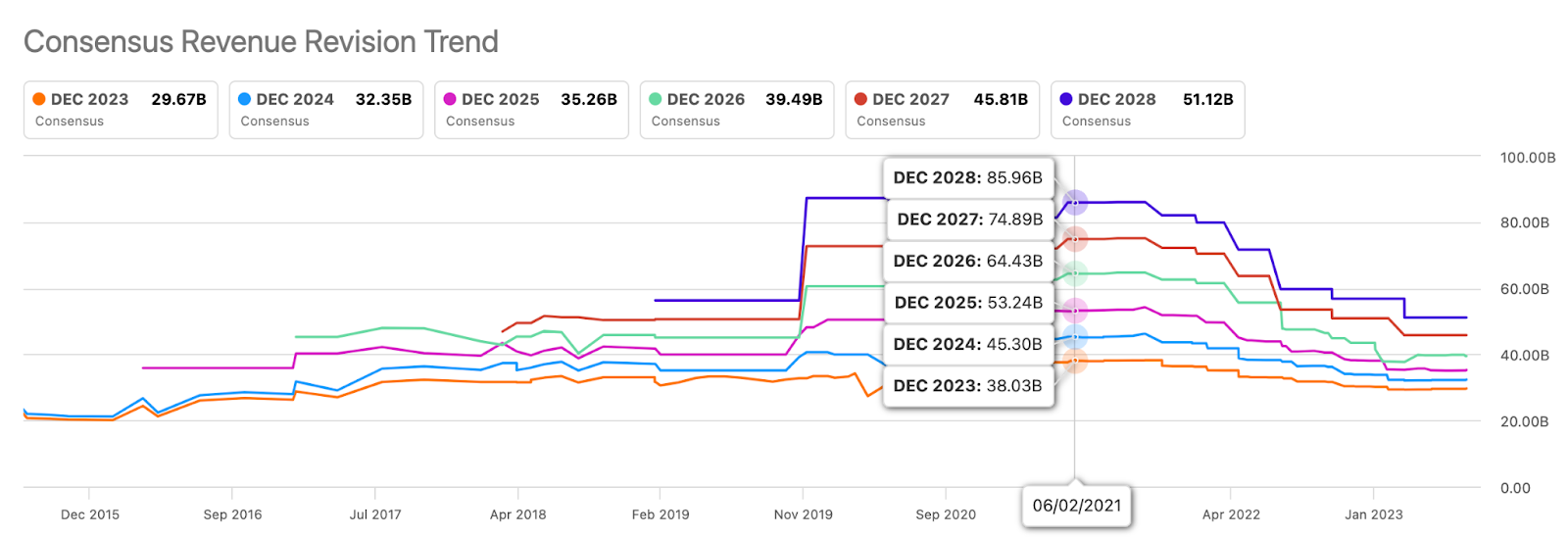

Source: SeekingAlpha, PayPal’s Revenue Revision Trend

Further, you can see that the consensus estimates for PayPal’s growth continue to decline.

|

Financial Year |

Estimates in 2021 |

Estimates in 2023 |

Difference |

|

2023 |

38.03B |

29.67B |

-22% |

|

2024 |

45.30B |

32.35B |

-29% |

|

2025 |

53.24B |

35.26B |

-34% |

Comparing 2021 to now, PayPal looks like a growth story that turned sour.

PayPal’s Margin Contraction

Source: Brad Freeman, Twitter (@StockMarketNerd)

Further, PayPal seems to have enjoyed short-term tailwinds from the pandemic which artificially boosted their margins during 2020 and 2021, and they are now normalizing.

PayPal’s Impending Leadership Renewal

It is also worth noting that Dan Schulman, CEO of PayPal is expected to retire this year and he will be naming his replacement in the coming months.

This transition, especially at the top, will rattle investors as it will be a source for huge uncertainty down the road. No one for sure knows what the new Chief Executive will bring to the table, and especially his/her track record.

PayPal Stock Analysis: Business Fundamentals

When investing, it is crucial to adopt the perspective of a business owner. Therefore, we should at least have a foundational understanding of PayPal’s business model/case.

How Does PayPal Make Money?

PayPal offers merchants an end-to-end payments solution and provides authorization and settlement capabilities, as well as instant access to funds and payouts.

They basically charge a fee for completing payment transactions for their customers and payment-related services, based on the volume of activity processed. This business model sounds increasingly attractive as they are able to scale with inflation and transaction volume, as long as they are able to retain both the merchants and users on their platform.

Further, PayPal offers other value-added services like interest and fees from merchant and consumer credit products, interest earned on assets, referral fees, subscription fees, getaway services and more.

Source: Quartr

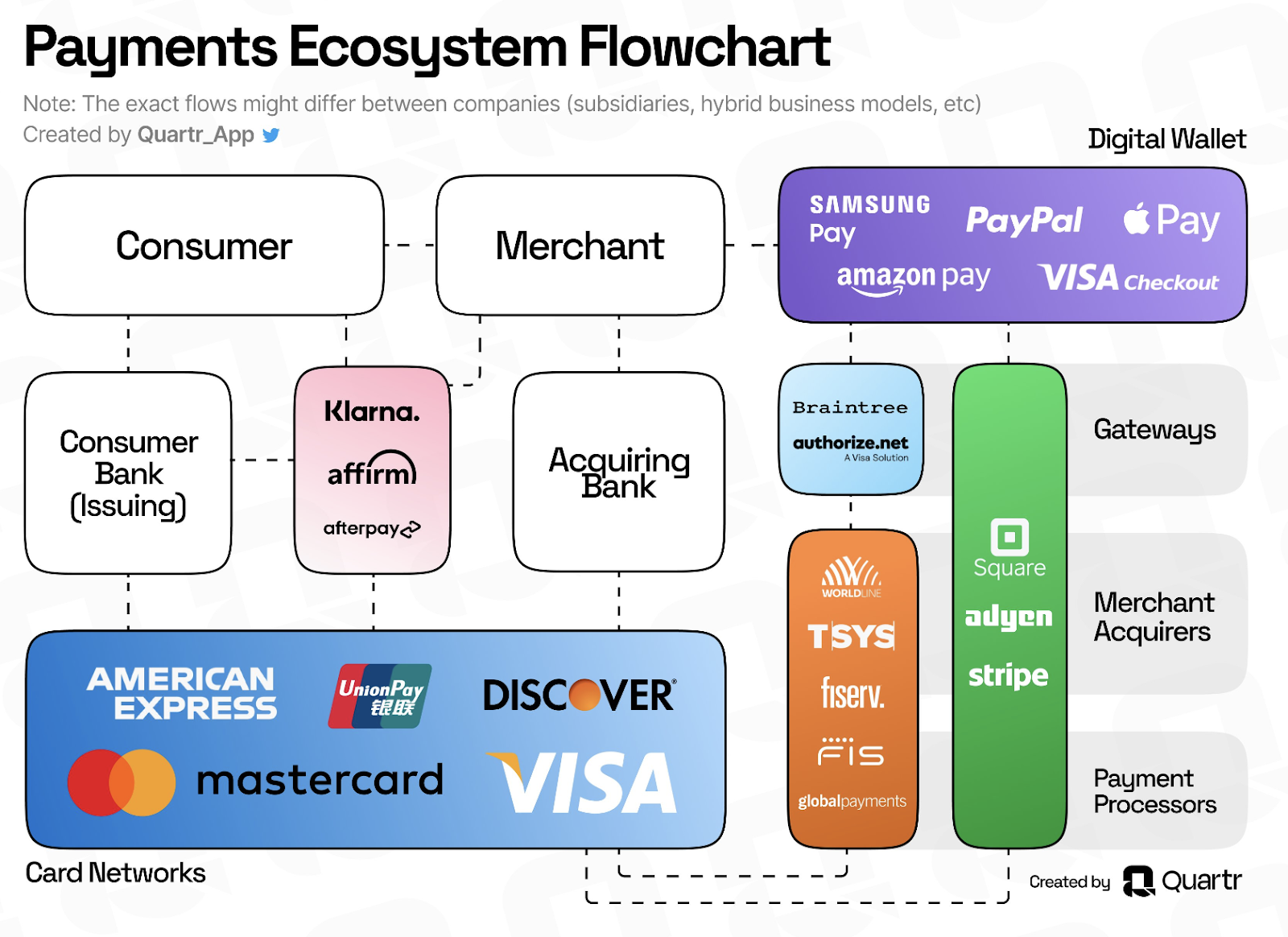

PayPal works effectively like a virtual cash register — they collect and encrypt transaction data and send that to the processor. A processor (like Ayden or Stripe) will do most of the heavy-lifting in the transaction process.

You will have to get yourself familiar with the payments ecosystem to have a better appreciation of PayPal’s moat, or lack thereof, which will be discussed in more details in the later part of this article.

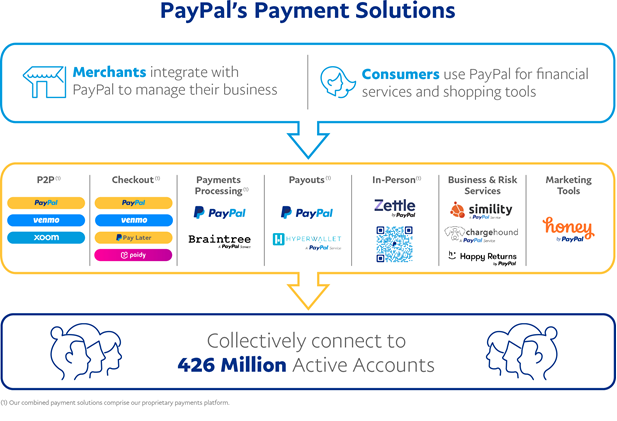

PayPal’s Main Business Arms

PayPal essentially has two main business arms: Branded and Unbranded Checkouts.

Source: PayPal’s 10-K 2022 Report

PayPal’s Branded Checkouts:

Currently, PayPal remains the leader of merchant checkout adoption, with more than 400 million total accounts and 100 million monthly active users on their platform.

Early investors were touting that this large consumer base works like a flywheel — as more consumers get onboard, merchants will more likely seek partnership with PayPal, and with the proliferation of PayPal payment methods, customers will be incentivized to maintain a PayPal account for the increased accessibility.

However, most have come to realize that this payment gateway industry is largely competitive with little to no differentiation. This is because a merchant is not bound to offer only one solution to their customers.

So the intuitive question would be, merchants will almost always want to switch over to the lowest-cost provider right?

Well… yes and no.

Yes, because which business owner would want to incur additional cost?

No, because it doesn’t seem like PayPal is completely losing its business and competitive advantage.

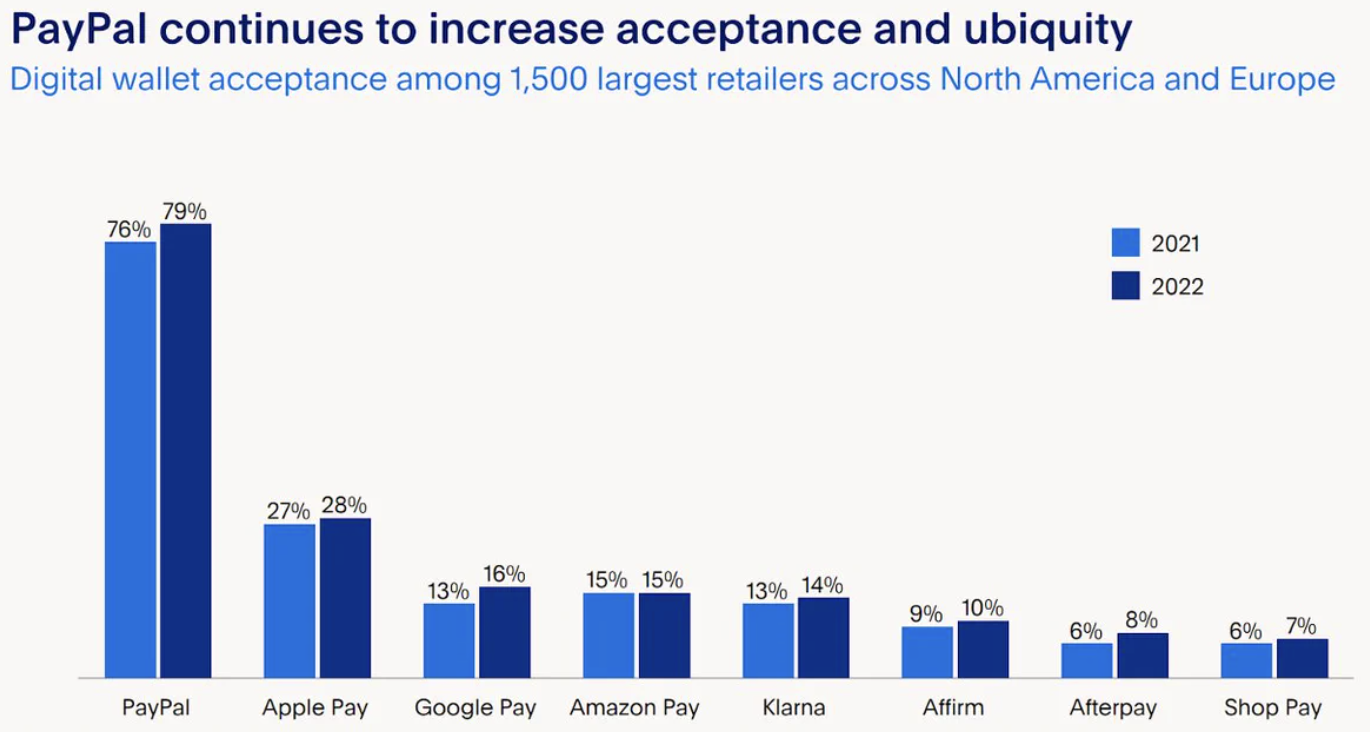

Source: PayPal Q4’22 Investor Update

In fact, PayPal gained another 3% of the checkout share during the pandemic amongst many strong players in the field like Apple Pay, Google Pay, Amazon Pay.

There are definitely more considerations than cost when it comes to choosing your preferred payment gateways. From PayPal’s perspective, they position themselves as being the best in protecting both the customers and merchants while delivering the highest conversion rates.

As per Neilsen (commissioned by PayPal to conduct a study), PayPal customers convert 2.8x more when shopping with merchants who accept PayPal - and they convert 28% higher at checkout, when compared to other payment methods.

Pew Research Center surveyed 6,000 Americans in late 2022 about money transfer preferences, and PayPal and Venmo took the top two spots for all age groups.

Currently, it does seem like there is some sort of elusive appeal to the PayPal brand that leads to better conversion numbers and trust amongst customers, which suggests why merchants are still sticking with them.

Venmo, which operates as a peer-to-peer (P2P) transaction platform, was also acquired by PayPal back in 2013. There have been many exciting developments, such as launching a crypto-transaction tool, a Venmo credit card, and even Venmo business profiles enabled by QR stickers.

Although PayPal managed to accrue a great level of interest and loyalty amongst the younger generation with the Venmo app, it still remains to be seen whether they can innovate and expand their product offering to convert these users to their higher margin offers. For now, Venmo does not add to PayPal’s bottomline in any meaningful way.

PayPal’s Unbranded Checkout:

PayPal’s unbranded business is Braintree — its entry into the white-label payment market. Essentially, not all merchants would gain from PayPal’s brand exposure but instead wish to retain control over their brand. Some notable brands like Uber, TikTok and Spotify operate with Braintree’s solution.

Fundamentally, this is not seen as an accretion for the overall business. On the bright side, PayPal branded checkouts do get to benefit from the new software stack Braintree offers, and they can integrate well.

However, PayPal’s foray into white-label processing and P2P also suggests that they are cannibalizing their core high-margin business.

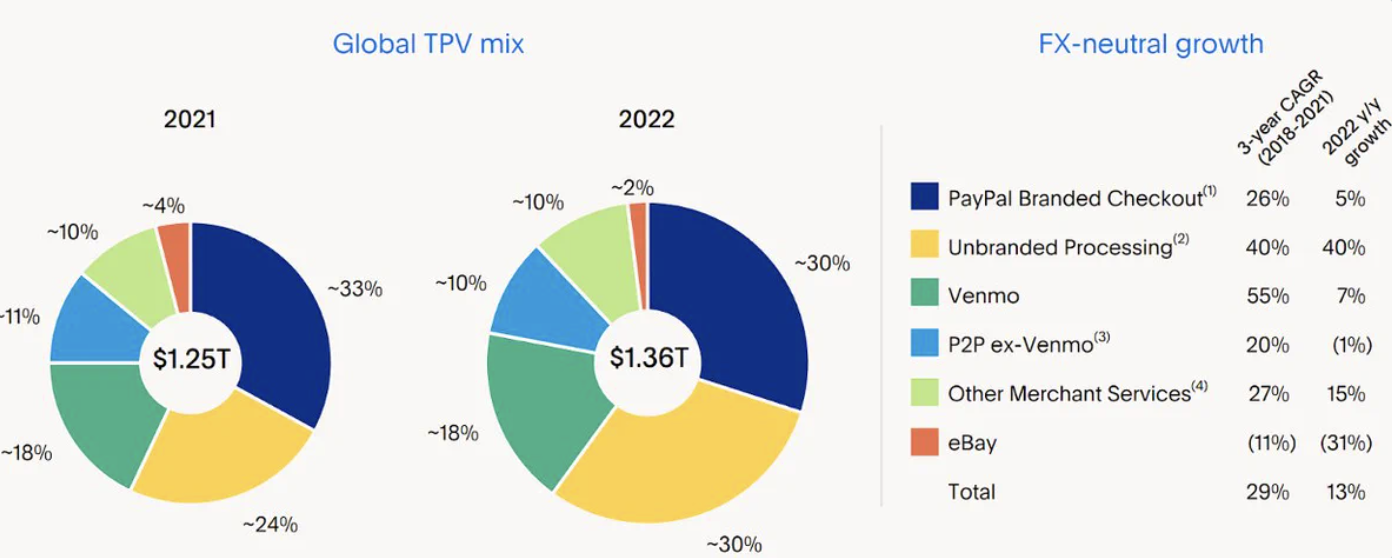

Source: PayPal Q4’22 Investor Update

You can observe that despite top line TPV (Total Payment Volume) growth still looking strong from 2021 to 2022, a majority of the growth is being fueled by lower-quality segments of the business; namely Unbranded Processing and Venmo (over the last 3-year CAGR), which contributes very little to PayPal’s bottom-line due to their comparatively thinner margins.

There is no doubt that businesses will be able to charge an arm and a leg for better perceived brand equity (as pioneered by Apple). But there needs to be a strong reason for customers to pay a much higher price to stay with you, and this story does not seem to hold in PayPal’s case.

Source: Brad Freeman, Twitter (@StockMarketNerd)

Despite the margin story of PayPal looking to fall apart, they have recently debuted the PayPal Commerce Platform as a targeted approach to enable and assist small and medium-sized enterprises.

Furthermore, with the current reach of Braintree, PayPal is focused on upselling other services like Hyperwallet (a platform that allows users to withdraw money from their WorkMarket platform to bank accounts outside of the US and Canada) — further enhancing the stickiness and reliance of users for a convenient experience.

Presently, with both their marketing and sales efforts, investors are hopeful to see whether they are able to deliver on both the growth and margins recovery.

Will PayPal Stock Go Up? My Problems with PYPL Today

Despite digging deep into PayPal throughout the course of writing this analysis, I still struggle to fully comprehend the unrivaled value proposition PayPal delivers to their customers.

Yes, many PayPal bulls will bring up several common counter-arguments:

- PayPal has solid authorization rates and world-class loss and fraud rates

- PayPal is currently the dominant leader in the space with no close second

- PayPal has access to troves and troves of data, touchpoints, customer spending history etc. so they are able to better conduct analytics and processing

All else said, the payment processing space is getting increasingly fragmented and competition is fierce, with companies trying to one-up one another.

Why PayPal’s Margins Are Decreasing at an Alarming Rate

The initial bull case of PayPal dominating the space is getting less relevant from their numbers.

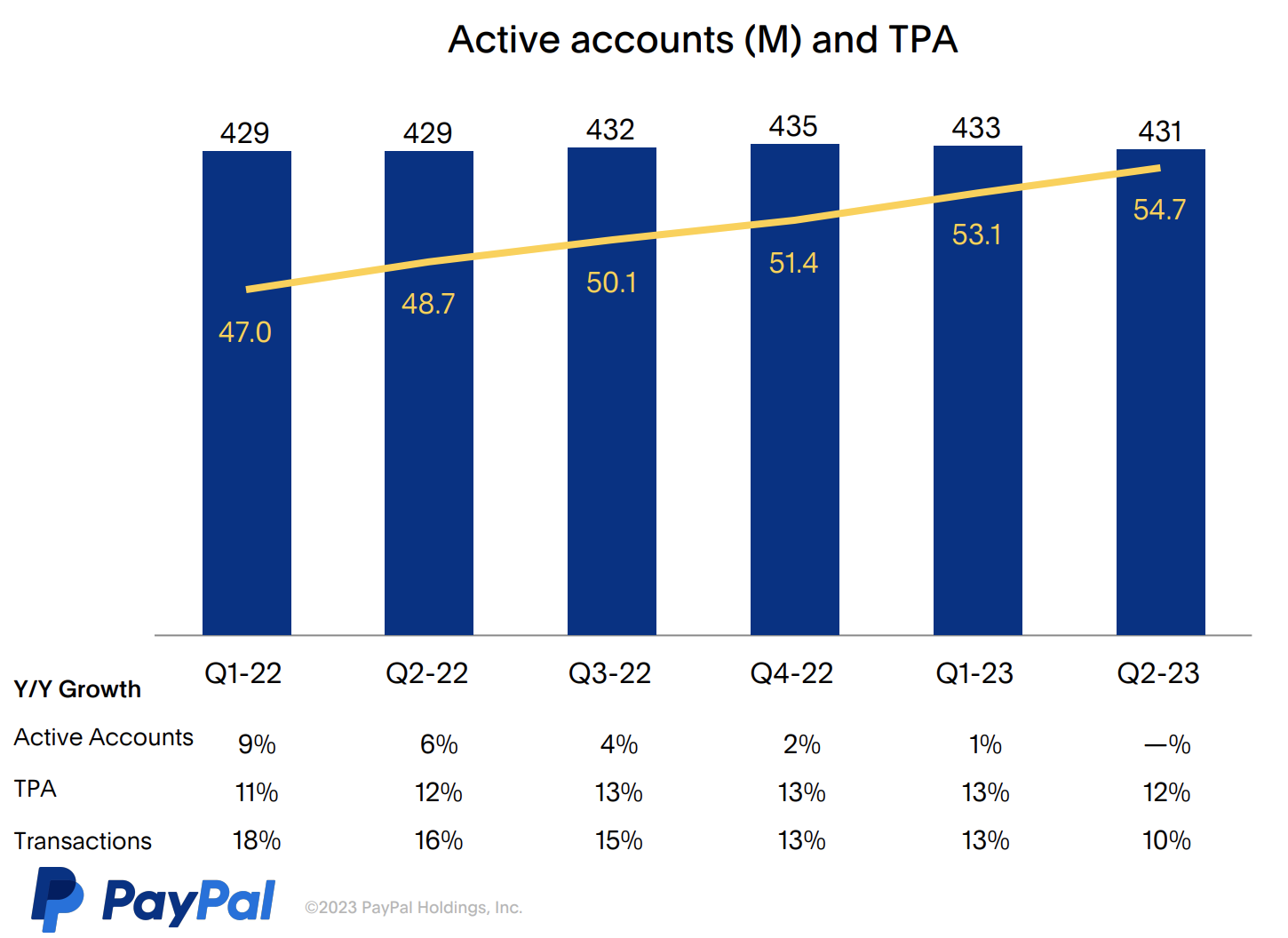

Source: PayPal Q2’23 Investor Update

As seen from their latest Investor’s Update, the number of active accounts is trending in a worrisome direction. In the payment processing industry, there are two ways to drive payment volume growth. Either through the addition of new accounts or users, or by driving the quantum of transactions per user.

At least in the short term, PayPal has recognized that they have hit a certain level of saturation and are now focusing on driving the engagement per user. It is also noted in their report that in the latest quarter, transactions have increased by 10%, and transactions per active account (TPA) have increased by 12%, which was primarily driven by Braintree transaction growth.

This suggests that PayPal’s core branded checkout is under heavy pressure (which also happens to be the high margin segment of the business).

Source: PayPal Q2’23 Investor Update

The worrisome trend of decrease in transaction take rate and total take rate, despite overall volume growing at the top, suggests lower-quality growth.

Along the way, PayPal’s dream to build a super-app was muddled in reality by many different acquisitions and expansions in adjacent product lines that have caused their margins to take a hit. Their EBITDA margins have fallen precipitously from 28.1% from the prior year to 24.6%.

PayPal’s Product Positioning in the Market Today

PayPal’s initial brand story was that they were the easy-to-use online checkout button that enabled quick and convenient checkout. In today’s context however, many larger enterprises are taking much more control over how they want to design and orchestrate their checkout procedure — hence, trying to eliminate the middleman.

Furthermore, even smaller merchants are seeking to increase the surface area to capture more customers that don’t happen to have a PayPal account by providing alternative payment methods. Compared to ten years ago, PayPal was highly valued for their convenience, fraud detection and prevention capabilities, but the advancement of the industry as a whole has enabled most other alternative providers to be able to match their core offering to a large extent (albeit sometimes falling short in some areas).

Let’s be clear, I’m not saying that this is THE END for PayPal. In fact, I’m saying the opposite. I still believe that there is a runway for PayPal’s relevance in the payment processing ecosystem as they have managed to retain many users that are still actively contributing and consuming within their ecosystem and have grown reliant on them.

What I’m arguing however is that based on this fragmentation trend, the allure of PayPal’s checkout button is slowly degrading.

In fact, in 2022, they have released a PayPal CashBack Credit Card, with their foray into the credit business.

Even with the introduction of a PayPal card, they are entangled with either partnering with Visa or Mastercard to enable transactions with the incumbent point-of-sale system.

Therefore, it is in our view that if an investor is really interested in having exposure in the payment processing space, both Visa and Mastercard are good stocks to explore.

To give you a flavor on their growth trajectory, using 2022 Total Payment Volume (TPV) figures:

- PayPal grew their TPV by 9% YoY to 1.36T

- Visa grew their TPV by 12% YoY to 11.6T

- Mastercard grew their TPV by 12% YoY to 8.2T

PayPal’s Dangerous Foray in Loaning

On the topic of extending credit to their customers, PayPal first engaged in Buy-Now-Pay-Later (BNPL) offers in 2020 under the program “Pay in 4”, whilst extending it to “Pay Monthly” in 2022.

Currently, PayPal merchants can opt into the BNPL program set out by PayPal at no additional cost and inconvenience to run them. They gain access to the more flexible payment options and need not assume any balance sheet risk.

This would then mean that someone else in the network has to assume this risk, and it would be PayPal. They will fund the transactions and store some of the credit on their own balance sheet.

The upside of course would come where BNPL as a consumption habit has enabled more conversions for the merchants. Presently, BNPL has delivered a consistent 21% increase in volume via higher conversions and larger checkout sizes. This volume explosion is beneficial to everyone in the network, arguably at the expense of the customers (because they tend to spend more, oops).

That said, the most worrisome part in my view is the dangerous game PayPal is getting themselves into, called “loaning”.

The loans business itself is a can of worms. From an accounting perspective, there are many level of consideration that needs to be taken into account, for example:

- The credit worthiness of the user that you extend the credit to

- The probability that the user will default on the payment

- What is the level of provision that you envision

- An ongoing assessment of whether the provision is sufficient

From an investor’s perspective, the outstanding loans will look good on the balance sheet as they will be accorded to the assets of the business. However, in bad times, there might be a need for high levels of impairment, which will have the reverse effect on the company.

For now, it does seem like PayPal is taking active steps to try and offset this liability to a third party through partnerships. In the latest earnings, they’ve announced a multi-year agreement to sell their European BNPL receivables to KKR3, where they expect around $1.8B of proceeds at close.

At the end of the day, in this quadripartite relationship between the customer, the merchant, the payment processor and the third-party dealer - there must be a balance of risk and mitigation. If one party is “significantly benefitting” from the relationship, it might mean that the rest of them are “footing for the bill”.

In this instance, the merchant and customer seems to be getting the benefits with no incremental cost on their end, while PayPal is assuming most of the risk, while at the same time transferring it to a third-party.

Introducing a third party into the picture does not make the risk magically disappear, and they would have to benefit from this relationship as well. PayPal has allowed for the loans to be sold at a discount to its face value for them to assume those risk on behalf of PayPal.

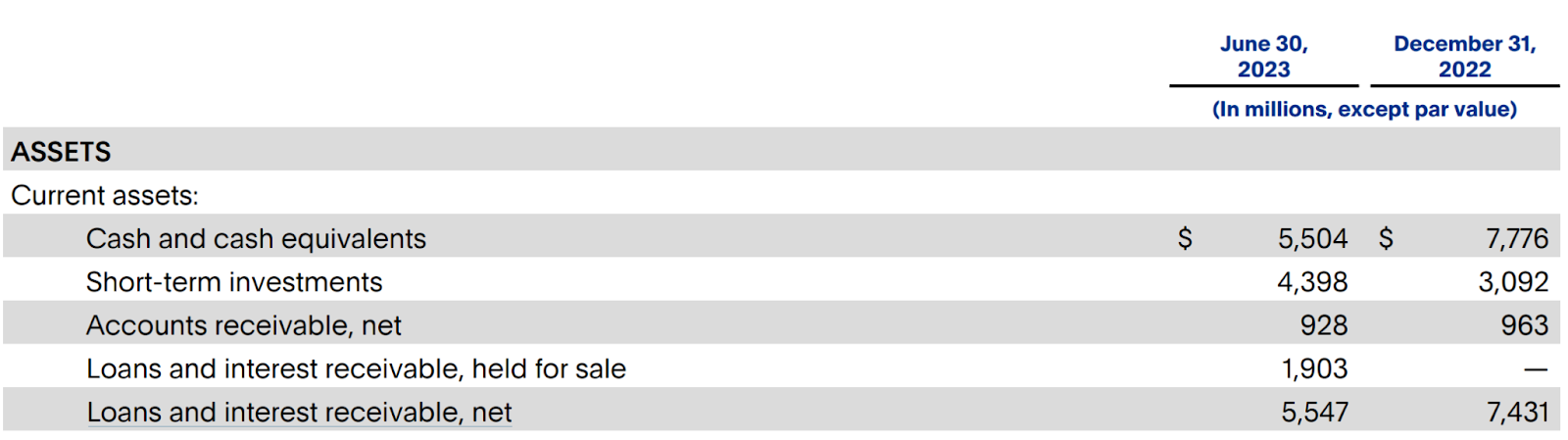

Source: PayPal Q2’23 Investor Update

Even after excluding the loans receivable held for sale, PayPal still has about $5.5B left on their balance sheet.

There is a very convincing argument to make on why PayPal should expand aggressively into the lending business (they “trap” people in their ecosystem as they become more reliant on the entire PayPal network). The bigger concern however, is how we should expect this loan business of PayPal to grow from here, and whether PayPal is able to mitigate the downside of most lending businesses in the long-term.

Is PayPal a Good Stock to Buy: Value Trap or Gem?

Many investors might then be wondering after our constant beration of PayPal — is PayPal still a good stock to buy?

Since you have stayed till the end of this article, we will give you the bottom-line of how we view PayPal stock as an investment today.

First, PayPal is not your random unprofitable, high growth tech company. They are probably not going to go bankrupt anytime soon, and they have been buying back shares at a much cheaper valuation from the company’s historical performance, coupled with a decent profit margin (albeit decreasing).

However, we will not be touching PayPal stock anytime soon because we are of the view that PayPal’s economic moat is experiencing some severe headwinds that might not be easy to correct in the short to medium term.

Furthermore, given the current impending leadership change that will arrive by 2024, we think it would be prudent to wait for the complete transition of the new CEO, and to give him/her time to execute of their vision / roadmap of the company before taking a long position (if we do observe signs of recovery and PayPal’s moat going in the right direction).

With that said, we will now take some time to elaborate on why many “value investors” seem to be jumping on the PayPal bandwagon, shouting it as a buy.

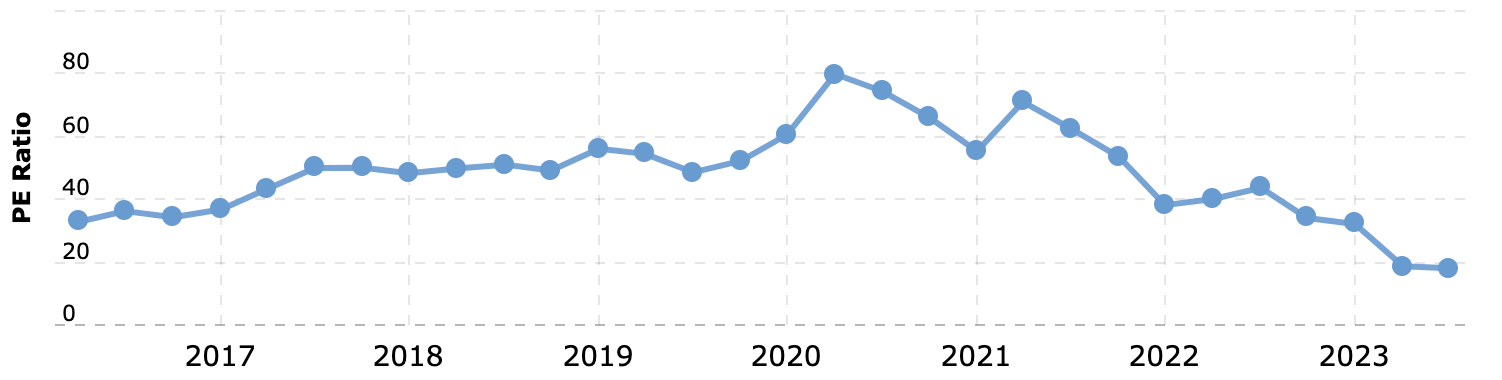

Source: Macrotrends, PayPal’s PE Ratio between 2016 to 2023

On a relative basis, PayPal’s Price/Earnings Ratio is currently trading at all-time lows. Historically, PayPal has traded at an average multiple of over 30x earnings since its IPO. Many would argue that with a debt-free balance sheet and growth (in the high teens) resuming, 20x might seem like a reasonable multiple for PayPal, whilst the current Forward PE of PayPal is hovering closer to 12x instead.

That being said, please keep in mind that the PayPal of 2023 is probably very different from the PayPal of the past.

Source: SeekingAlpha, Consensus Revenue Estimates for PayPal

Source: SeekingAlpha, Consensus EPS Estimates for PayPal

You can clearly see that Wall Street’s expectations for PayPal’s upcoming top-line growth rates in the coming three years have been heavily muted, and a high single-digit revenue growth might no longer be able to command the 30x PE multiple that they used to have.

That said, many investors are excited about the bottom line implosion, where they are expected to accelerate much faster than revenue growth, because it seems like PayPal is on a mission to gobble up their outstanding shares.

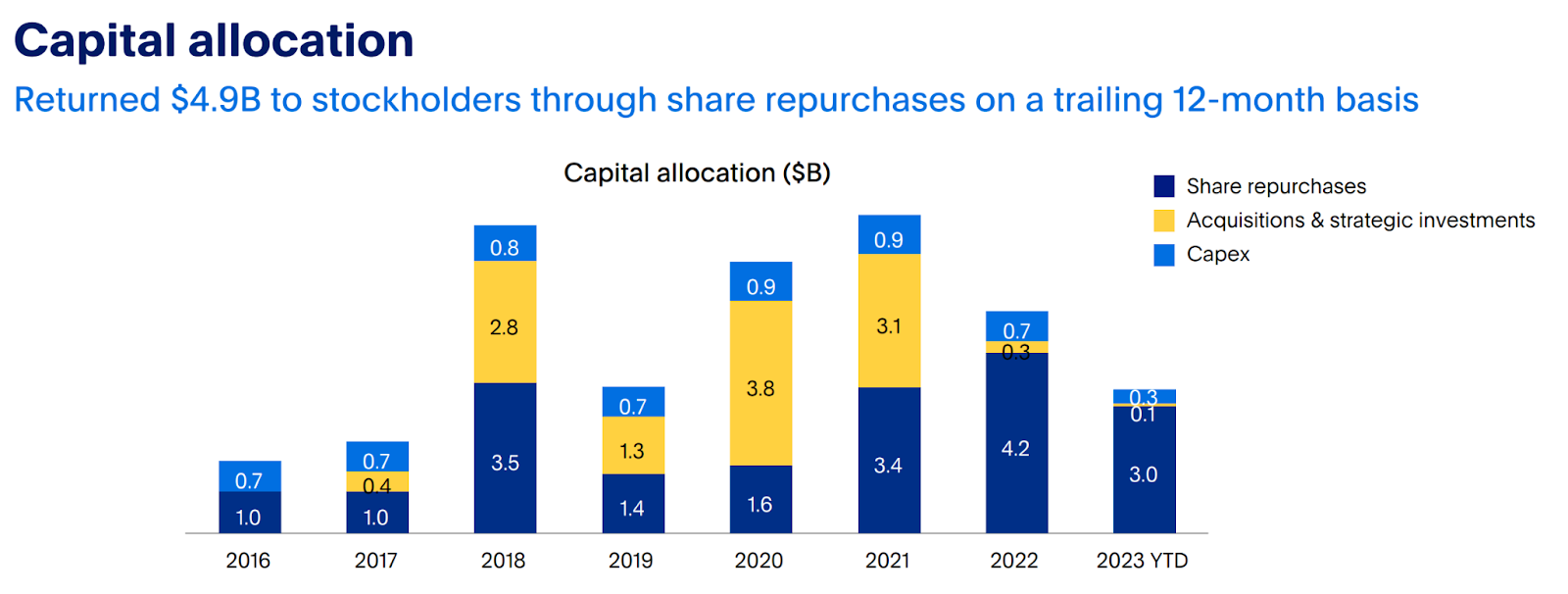

Source: PayPal Q2’23 Investor Update

On a trailing 12-month basis, they have returned a grand total of $4.9B to shareholders by repurchasing around 63 million shares. Since 2019, the trend of share repurchases have only gone in one direction, which is up, and this is probably exciting news for investors.

For context, PayPal’s current valuation hovers around 70B to 75B. At the rate at which they are extinguishing their shares, if they continue to increase their buybacks at this pace, they might very well be able to repurchase all of their shares within 10 to 12 years.

Source: PayPal Q2’23 Investor Update

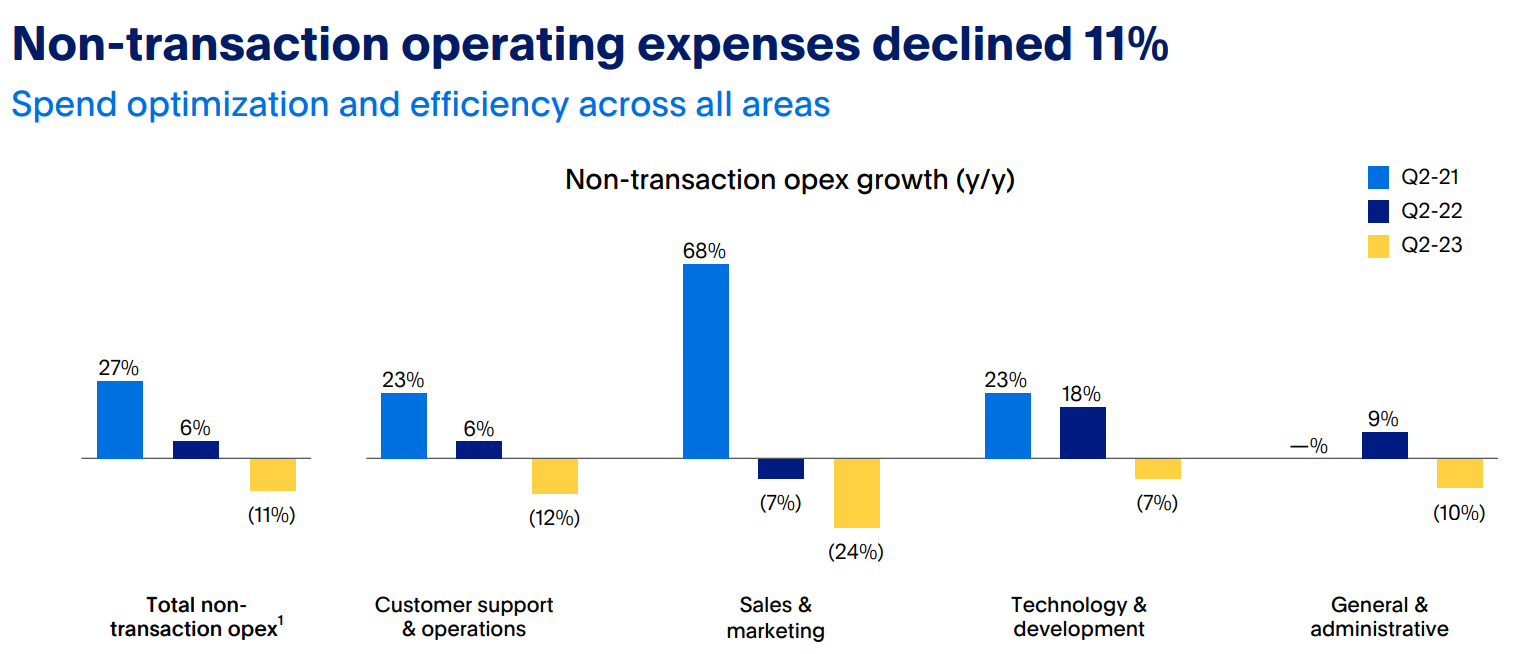

Also, PayPal seems fairly determined in getting their cost structure in line, suggesting that there is even more upside investors can expect as there will be a continuous improvement on the margin front, and also the bottom line shareholders can expect.

Conclusion

Reducing cost, driving strong bottom line growth, buying shares back aggressively… no wonder many investors are interested in PayPal stock.

Despite feeling upbeat about the potential prospects of aggressive share repurchases and earnings reversion, we still do not feel comfortable allocating capital to PayPal for the following reasons:

- Fundamentally, we still believe that PayPal’s moat is significantly challenged in an ever-fragmented market

- A company needs to have a long-term competitive advantage to be able to enjoy sustained earnings growth (which can then be returned to shareholders)

- Despite PayPal looking relatively cheap today and their aggressive buyback strategies, we are much more concerned with their longer-term outlook, margin profile and profitability trend

- We do not want to be held hostage by management’s discretion of buying back shares, which is not guaranteed, suggesting that the EPS growth might be stalled

- We are unsure of the game plan of the incoming CEO

For these reasons, we’re out for now.

If you are interested to find out companies with wide economic moats that are currently in our portfolio or watchlist, do check out the Ultimate Investors Playbook where Adam Khoo has done deep-dive analysis of the competitive landscape, financial performance and valuation framework around many strong potential stocks.

Till the next time, Keep Winning.

submit your comment